Europe’s Carbon Border Adjustment Mechanism (CBAM) has moved from concept to action. Since October 2023, importers of iron and steel—including stainless—must report the embedded emissions of what they bring into the EU. From 2026, those disclosures turn into carbon costs linked to the EU Emissions Trading System price.

For stainless steel users, this isn’t a niche policy debate. It is a practical shift in how stainless is specified, purchased and reported. The upside is real: a market that rewards use of low-emission materials and puts a fair price on carbon emissions both for imports and producers in Europe. However, this progress does not close the gap – important loopholes remain, and further policy action is needed to ensure CBAM delivers on its intent.

As imported stainless steel can include carbon emissions five times higher than European stainless steel, there can be significant benefit in prioritizing the carbon footprint in procurement.

The global transition is underway

CBAM is not aiming to tackle only European industrial transition—it’s part of a broader shift to make carbon costs visible in global trade. Around the world, carbon pricing instruments now cover roughly a quarter of greenhouse gas emissions, and recent climate summits have accelerated this change.

For example, the Open Coalition on Compliance Carbon Markets was established during COP30 in Belém, Brazil, with the aim of integrating global decarbonization initiatives and establishing a common carbon pricing framework among countries.

For stainless steel users, this global signal turns procurement into strategic transition. Two coils that meet the same mechanical specification can carry very different embedded emissions, driven by production route, technologies used, electricity mix and choice of raw materials—and those differences now show up on the bottom line.

For more than a decade, European stainless steel producers have carried a carbon cost that many foreign competitors did not. Under the EU ETS, mills paid for their emissions while imported steel faced no equivalent price at the border. While free allocation softened the impact, it never erased the imbalance which penalized cleaner European producers as higher emission imports undercut on cost.

CBAM finally corrects this imbalance. From 2026, imports will face the same carbon signal as production inside the EU. Paired with the phase out of free allowances, this restores a true level playing field—good for both climate integrity and for Europe’s industrial base.

From policy to procurement: what CBAM really means for stainless steel

To understand the practical implications of CBAM on stainless steel, we can answer three questions: who, what and when.

The “who” is the EU importer of materials, now responsible for reporting and buying CBAM certificates from 2026. If you import coils, flats, long products or fabricated components directly, that maybe you; if you buy via a distributor, expect data requirements and costs to cascade through contracts and prices.

The “what” is embedded emissions—the greenhouse gases released during production before the product crosses EU customs. For iron and steel, the Commission has set rules for calculating those emissions at installation and product level. During the transitional phase, real company‑specific data is expected where available; if it isn’t, country-specific default values apply.

The “when” is now. The quality of reporting in 2024–2025 will shape baselines and processes. Payments start in 2026 as free allocation under the EU ETS is phased out in parallel for EU producers. You still have time to make the shift—but no time to wait.

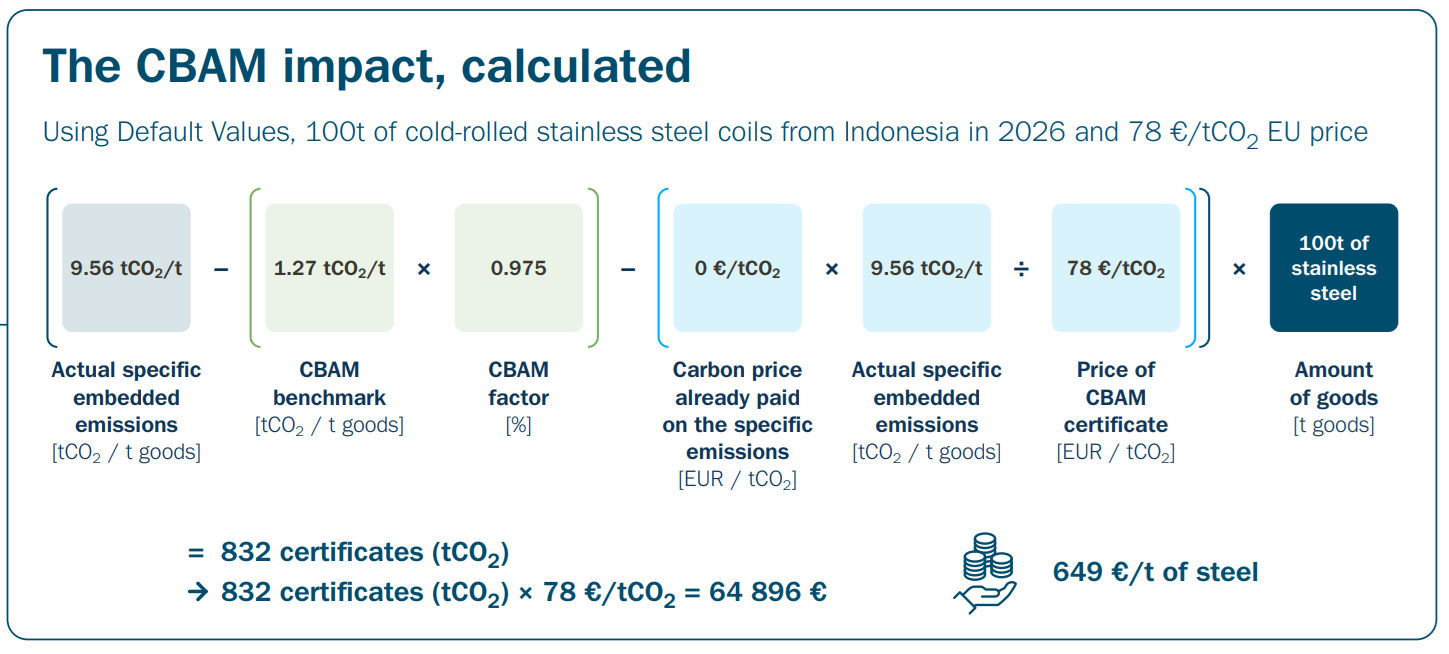

Here’s a look at how the costs can be calculated, using Default Values as an example:

As you can see in the example, the cost impact on steel coils from Indonesia, using the EU’s Default Values, is 649€ per ton of steel. Meanwhile, Outokumpu stainless steel produced in the EU is already covered by the EU ETS—and therefore faces no CBAM costs. You can watch our webinar on CBAM and stainless steel here for a deeper look at this topic.

The downstream ripple effects across stainless

CBAM turns emissions from an ESG footnote into a cost driver, and the effects will be visible at every node of the stainless value chain. Distributors will find that emissions transparency becomes part of the offer. Customers will increasingly ask for product‑level carbon footprints, verification statements and origin details; many will want to differentiate inventory by embedded emissions just as they do by grade or surface finish.

Automotive and heavy‑industry buyers will embed carbon attributes alongside alloy, quality and cost; contracts will favor suppliers who can deliver verified data at heat, batch or product‑family level, with penalties where defaults are triggered. Consumer goods and appliance brands will converge on low‑emission stainless to manage both CBAM exposure and credible consumer‑facing claims.

Non‑EU processors selling into the EU will likely see their EU customers press for installation‑level data to avoid default values; minor processing to change customs codes is not a strategy as anti‑circumvention rules are tightening. And EU fabricators using imported semis would need purchasing, logistics and finance to work off the same data so that CBAM declarations match invoices and shipments.

Additionally, there are still gaps that CBAM must address – especially corresponding measures for downstream segments. Without it, there is a risk that manufacturing shifts outside the EU, where finished goods can be produced and imported without equivalent carbon costs. In that scenario, Europe would retain neither steel production nor downstream value creation, undermining the broader objective of CBAM.

Outokumpu: helping you drive this change

As an industry, we have a chance to turn this from a compliance sprint into a competitive edge. The companies that integrate emissions data into purchasing now—without disrupting existing operations—will be the ones who control costs, meet customer expectations and move faster on their Scope 3 goals.

Product footprints vary widely by producer; at Outokumpu, our average product carbon footprint is 1.6 kg CO₂e per kg of stainless steel versus a global average of about 7 kg CO₂e/kg. This translates to a real financial impact.

Our role at Outokumpu is to make this shift practical while providing stainless steel with an up to 75% lower carbon footprint than industry average – with the ability to push down to 93% lower with Outokumpu Circle Green®.

We also provide product‑level carbon footprints for our stainless grades, built on robust methodology and third‑party assurance; standardized documentation that simplifies life for importers and distributors; and technical sessions to help teams integrate carbon data into ERP and procurement processes.

Want to learn more about CBAM and stainless steel? Download our CBAM fact sheet here or read our FAQs for more details – or register to view our CBAM webinar.